(Bloomberg) — Microsoft Corp. is at the intersection of two troubling trends roiling the technology sector, which has the stock on track for its worst quarterly performance since the global financial crisis two decades ago.

First, the software giant is doubling down on capital expenditures as Wall Street increasingly asks when investments in artificial intelligence infrastructure will produce more dramatic payoffs in revenue growth. And second, investors are selling software stocks over fears that AI startups like Anthropic and OpenAI are creating agents that can replace products made by companies like Microsoft.

“There is this concern that rather than paying Microsoft, we’ll see more customers go directly to AI vendors, which could disrupt the core business, or at least pressure pricing and margins,” said Jonathan Cofsky, portfolio manager at Janus Henderson Investors, which holds the shares.

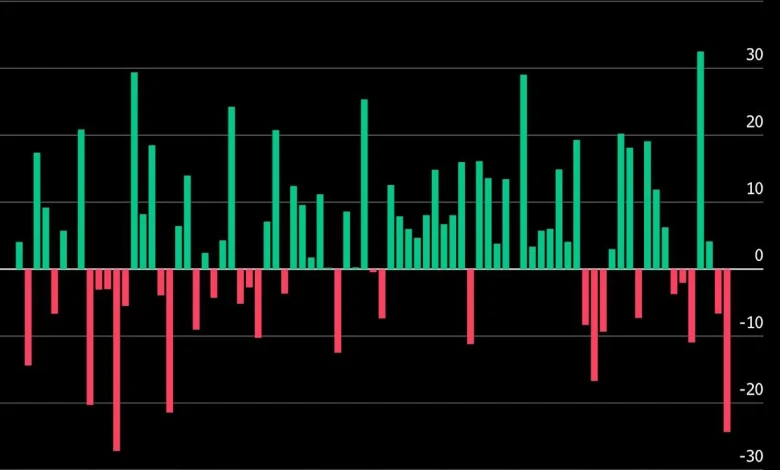

The company’s stock is down 25% in the first quarter, on pace for its biggest loss since its 27% drop in the fourth quarter of 2008. It’s by far the weakest performer among the Magnificent Seven tech giants to start the year, with an index tracking the group falling 14% over that time.

Microsoft fell 1.7% after the market opened on Friday, putting it on track for a fourth straight session in the red.

“Microsoft has become a lot more capital intensive,” Cofsky said. “For the shares to perform better going forward, we need to become more comfortable that software growth won’t materially decelerate.”

The selloff has the stock looking relatively cheap, trading at less than 20 times earnings over the next 12 months, the lowest since June 2016. Microsoft’s multiple is slightly above the S&P 500 Index’s, and it recently traded at a discount to the broad equities benchmark for the first time since 2015.

Although Wall Street remains optimistic that it will emerge as a long-term winner from AI, Microsoft still has to keep up with the hyperscaler spending race, a posture that could complicate any near-term sentiment reversal. The company’s capital expenditures, including leases, are projected to reach $146 billion in fiscal 2026, which closes at the end of June. That’s up about 66% from $88 billion in fiscal 2025, and the figure is expected to swell to $170 billion in fiscal 2027 and $191 billion in fiscal 2028, according to the average of estimates compiled by Bloomberg.

Investors are increasingly taking a jaundiced view of that kind of spending, especially without a more pronounced acceleration in growth. In its most recent quarterly results, Microsoft’s closely watched Azure cloud-computing division posted a slight deceleration in growth from the prior quarter. Meanwhile, Microsoft’s Copilot AI offering has gotten limited traction from users, leading it to shake up its AI operations to improve the service.

These issues reflect the mounting headwinds facing the company, according to Ben Reitzes, an analyst at Melius Research who has a hold rating on the stock. “Microsoft’s upside in Azure is capped as it scrambles to fix Copilot and its own models — and that doesn’t end in just one quarter,” he wrote in a March 23 note to clients.

Of the 67 analysts tracked by Bloomberg who are covering Microsoft, 63 have buy ratings, while three have holds and one rates it a sell. The average 12-month price target on the stock of $592 projects more than 64% upside over the next year. That’s the highest implied return on record, according to data compiled by Bloomberg that goes back to 2009. The stock is also trading under its 200-day moving average by the widest margin since 2009.

To Reitzes, the preponderance of buy ratings on the stock reflects complacency on the part of his Wall Street rivals. He sees additional risks for the company’s productivity and business processes segment as well as its More Personal Computing unit.

On the opposite end of the spectrum is Tal Liani, an analyst at Bank of America. He reinstated coverage on the stock with a buy rating earlier this week, citing Microsoft’s “durable multi-year growth across cloud and AI.”

Those two views really get to the heart of the tension surrounding Microsoft shares. The long-term outlook is hopeful, but there are very real execution risks between now and then. Whether those concerns are prescient or represent a buying opportunity is in the eye of the beholder.

“I think the stock has a lot of long-term value,” said Jake Seltz, portfolio manager at Allspring Global Investments, which owns the shares. “Its AI strategy will ultimately be vindicated, and I think it is largely insulated from the biggest AI disruption fears. In the meantime, those concerns are creating an opportunity, especially if you’re willing to have some patience.”

More stories like this are available on bloomberg.com

©2026 Bloomberg L.P.