The central bank’s regular economic updates project the short-term prospects for the economy using models tuned as realistically as possible. These updates do not usually delve into discussions of long-term economic strategy, which is the rock base on which the country’s future prosperity rests.

The latest Central Bank of Malta (CBM) economic update signals some positive prospects, however, tempered by sobering caveats about what could derail the sound prospects being forecast.

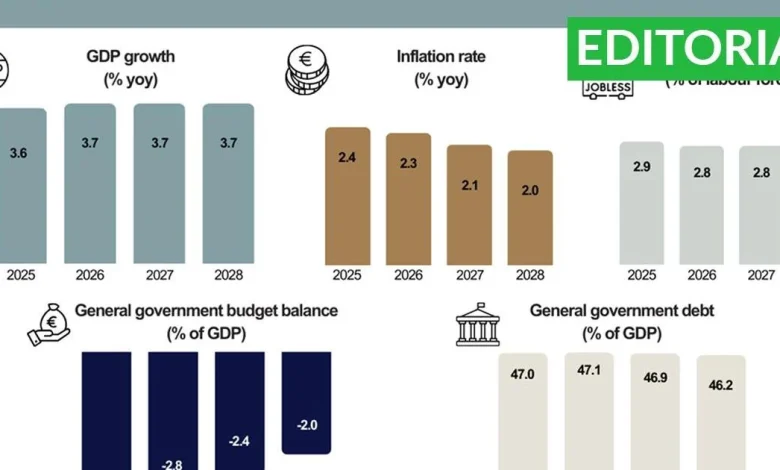

The headline signal is that Malta’s GDP growth is set to remain stable at 3.7%, a rate higher than most EU member states.

The government debt-to-GDP ratio is expected to fall to 46.2% by 2028, while inflation should fall to 2.0%.

However, the CBM warns that, in the current geopolitical scenario, there are risks that must not be underestimated, as they could adversely affect the economy more than anticipated. Malta has one of the most open economies in Europe, which means that events far from our shores, beyond our influence, could ultimately affect us.

The CBM is right to highlight that the international economic environment, along with elevated geopolitical uncertainty, can pose risks beyond our control.

While strong economic growth continues to be fuelled mainly by private consumption, this is leading to wage inflation, especially in the services sector.

Moreover, high food inflation, which is becoming endemic, could rise higher than expected amid adverse climate change.

Perhaps even more worrying is the trade uncertainty created by the tariff war, which shows no sign of abating. It is still unclear what effect international trade tensions will have on the prices of the goods we import.

While the current fiscal management is adequate, the risk of cost overruns over the next three years must not be underestimated. The government continues to ignore the advice of the International Monetary Fund and the European Commission to make the energy subsidy scheme more targeted to help lower-income families. If energy prices rise more than the CBM forecasts, it could mean the cost of subsidies will continue to rise.

Moreover, wage inflation keeps rising as the unemployment rates continue to decline and controls on imported labour become rather more evident.

For more than a decade, short-term economic indicators have been encouraging, outperforming those of most EU countries.

Of course, the flipside of this narrative is that economic growth is being driven primarily by low-value-added economic activities supported by low-cost labour, most of which is imported from third countries. Investment in human capital and high-end technology remains inadequate.

Moreover, the appetite for educational reform to prepare the country’s future labour force for the challenges of tomorrow’s economy remains low.

Educational reform remains the single most important factor in making the economy more dependent on productivity improvements.

There is no shortage of recommendations from the IMF, rating agencies, and the Commission on the need for Malta to reduce its reliance on an ever-increasing supply of imported low-cost labour to sustain its services industries, especially tourism. Ironically, the CBM’s positive short-term forecasts are more likely to encourage the government to stay in its comfort zone and shy away from the socio-economic reforms the country so badly needs.

If economic restructuring is postponed indefinitely, leaving the county with no choice but to do so, the change management process will become even more painful.

The geopolitical risks highlighted in the CBM report are undeniably out of our control. Still, the economic reforms necessary to prepare our younger generations for tomorrow’s economic realities will always be our responsibility.

Today’s political leaders owe it to tomorrow’s generations to manage the change that the country so badly needs.