Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

The day after the war with Iran began, I put out a post on what this meant for markets. I’m following that up today – as the US and Iran approach a negotiated settlement – with what’ll happen to markets once this conflict finally ends. Oil prices will fall sharply and quickly. As a result, markets will stop worrying about inflation and return to pricing cuts for the Fed. This means USD will fall rapidly, especially versus emerging markets (EM). We’re basically going back to the pre-war playbook of Dollar weakness and Fed cuts.

-

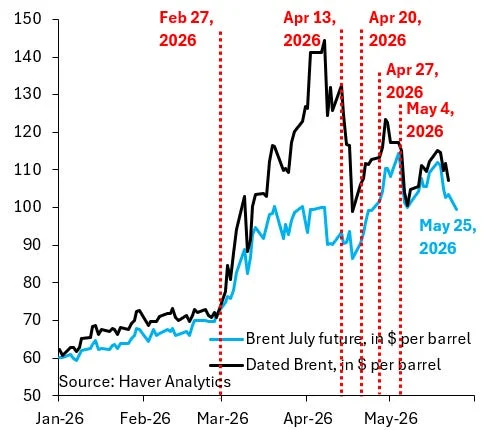

Oil prices will tumble. As the chart above shows, the Brent oil price started the year around $60 per barrel. We’re obviously not going back to that immediately because it’ll take time for ship traffic through the Strait of Hormuz to normalize, but markets are also forward-looking, so they’ll front-run a good amount of what actually happens in the Strait. If we tomorrow get a credible peace agreement, for example, I’d expect the front-month Brent futures contract to fall from its current level of $100 to $85 in fairly short order. We’ve seen similarly-sized drops on past peace deal speculation, so – if anything – this estimate might be conservative.

-

Markets will return to pricing Fed cuts. The black line in the chart above shows the Fed’s policy rate and the blue line shows what markets price for this rate at the end of 2026. The rise in oil prices following the start of the war saw markets quickly price out rate hikes and – more recently – they began to price hikes. This is going out the window as soon as we get a peace agreement. As I flagged in a recent post, there’s no sign that underlying inflation is picking up, so no reason for the Fed to hike. If anything, we’ll quickly return to markets pricing Fed cuts.

-

The Dollar will fall. The black line in the chart above is the 2y2y forward rate differential of the US versus its G10 peers. This 2y2y forward tenor proxies for where markets see the terminal rate in the US versus the G10, which moved sharply in favor of the Dollar in recent weeks as Fed pricing shifted towards hikes. If markets shift back to pricing cuts, the black line will return to where it was before the conflict, which’ll drag the Dollar versus the G10 down (blue line). I continue to see the biggest scope for the Dollar to fall versus EM. As the black line in the chart below shows, it’s here that the decline in the Dollar has been most pronounced and – once the war ends – we’ll go back to having this as a dominant markets theme for the rest of 2026.

My bottom line is that we’ll quickly go back to the playbook from before the war. The implicit assumption I’m making is that the conflict leaves little lasting damage. There will be some – fiscal space has been eroded further, so long-term yields won’t retrace entirely to where they were before the conflict – but that shouldn’t alter the playbook for Fed market pricing or the Dollar.