Thank you for subscribing to my posts. If you’re not yet a paying subscriber, please consider becoming one. That’ll allow you to DM me with questions and comments. I plan to move my posts behind a paywall in coming months. Subscribing now locks you in at a low rate. Thank you so much for your support and feedback!

On Monday, I put out a post on what markets will do when we get a peace deal that – critically – reopens the Strait of Hormuz. At the time, the front-month futures price for Brent was around $100 and I said we’d go to $85 in fairly short order. We’re now around $90, so we’re well on our way towards that target.

Beneath all this lies a bigger question on what constitutes “normalization.” After all, even under the best of circumstances, it’ll take time to get tanker traffic through the Strait back to normal and – in reality – it’s likely that Iran’s hard liners will attempt to sabotage a peace deal, including by lobbing rockets at transiting ships. As a result, it’s unlikely that oil prices will return to the status quo ex ante any time soon. Some risk premium will have to remain. Moreover, as Ben Harris and I flag in a recent blog, lots of temporary supply buffers that helped cap oil prices are now almost depleted, so a risk premium will also be need for that.

My focus in this post is on what constitutes “normalization.” I start by documenting where normalization has already happened, which is – to a substantial degree – in the recoupling of regional oil markets around the world and the disappearance of the gap between “physical” and “paper” oil prices. I then discuss the kind of risk premium that should stay priced – even with a peace deal – and how quickly gas prices at the pump can be expected to normalize.

-

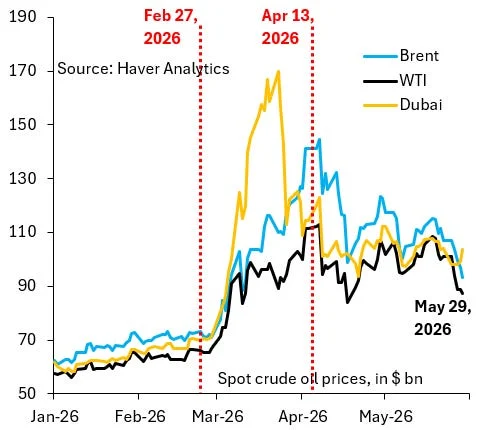

Recoupling of regional oil markets: ordinarily, benchmark crude prices from around the world move closely together, which is what the chart above shows. But the start of hostilities and the closure of the Strait meant that Dubai crude – the benchmark price for Asia – shot up as panic gripped the region. This decoupling of regional oil markets ended several weeks ago, signaling abating stress and normalization.

-

Recoupling of “physical” and “paper” oil: the start of the war saw “physical” prices rise far above “paper” prices, which the chart above shows with the widening gap between the black and blue lines. At the time, overwhelming consensus was that this gap would close with futures rising towards spot prices, but – in the event – the opposite happened. Spot prices fell towards futures. Another sign of normalization in oil markets.

-

What kind of risk premium stays: in my chat with Paul Krugman on his podcast on March 19, I discussed the risk premium by comparing the Brent spot price to where it was – at a similar moment in time – after Russia’s invasion of Ukraine. My basic point was that the Strait of Hormuz is roughly three times as important as Russia for global oil markets and that Brent – at the time – had risen way more than three times its 2022 rise. As a result, the case for oil prices to go a lot higher wasn’t particularly compelling. Where does this logic point now? We’re now up twice as much as in 2022 on a similar time scale, which – if we get a peace deal – seems too much and in my opinion suggests there’s room for Brent to fall somewhat further. $85 or slightly below seems like a decent target.

-

Gasoline prices at the pump: there’s a relatively close relationship between the US’ national average gasoline price (black line) and the price of the August Brent future (blue line), as the chart above shows. If Brent continues its fall forwards $85, it’d be reasonable to expect prices at the pump to fall back – with a lag of a few weeks – to four Dollars a gallon. The sooner prices at the pump come down and this whole episode is in the rearview mirror, the better for the Republicans in November. This I think is the strongest argument for wrapping things up quickly.

It’s reassuring that “normalization” has already happened along several dimensions. The global oil market isn’t as broken as it was in the early days of the war. If Brent falls to $85, which would still leave a substantial risk premium, that should see gas prices at the pump gradually fall back to $4 a gallon. This would be normalization.